Market Recap

The final quarter of 2023 delivered a strong Santa Claus rally across most major asset classes with commodities being the lone outlier (see chart below). The S&P 500 index finished the year just short of surpassing its record high set back in early 2022, as optimism around softer inflation data and future interest rate cuts helped ease recession concerns. From a style perspective, growth stocks once again outperformed value, as the ‘magnificent seven’ tech and AI stocks continued to dominate broader stock market returns. Outside the U.S., developed and emerging market equities also delivered strong returns for the quarter as hopes for interest rate cuts in early 2024 bolstered risk sentiment.

Global fixed income markets were positive across the board in the fourth quarter. Falling inflation and increased expectations for central bank rate cuts drove prices higher on assets with greater interest rate sensitivity such as government bonds. Meanwhile, more speculative areas of fixed income such as high-yield and emerging market debt also performed well, as recession worries faded and most global economies showed surprising resilience.

| Q4 2023 | Trailing 12 Months | Trailing 3 Years | Trailing 5 Years | |

| S&P 500 | 11.69% | 26.29% | 10.00% | 15.69% |

| Russell 2000 | 14.03% | 16.93% | 2.22% | 9.97% |

| MSCI All Country World Ex-US | 9.75% | 15.62% | 1.55% | 7.08% |

| Bloomberg US Aggregate Bond | 6.82% | 5.53% | -3.31% | 1.10% |

| Bloomberg Commodity Index | -4.63% | -7.91% | 10.76% | 7.23% |

| Dow Jones Comp. All REIT Index | 17.56% | 11.46% | 5.33% | 7.14% |

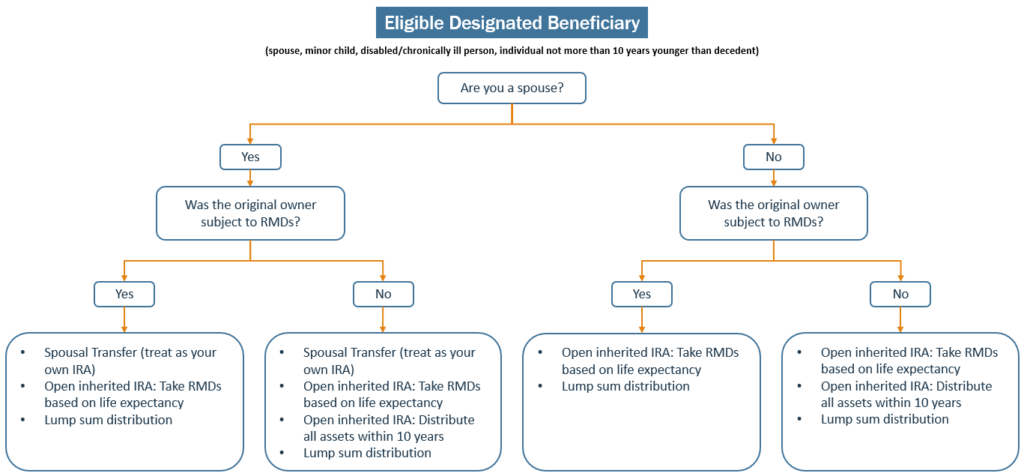

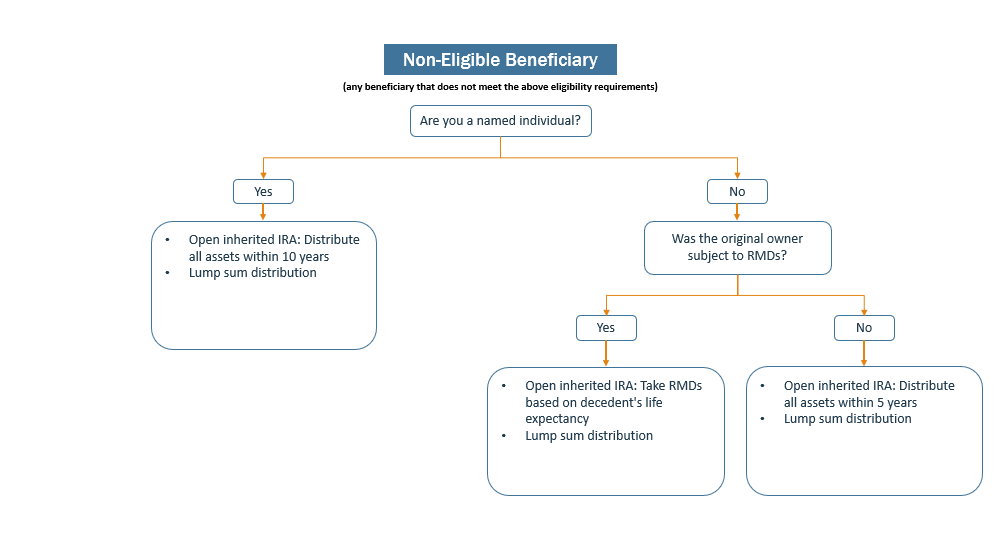

Inherited IRA Withdrawal Rules (Post SECURE Act)

Over the next two decades, baby boomers and the silent generation are expected to transfer roughly $84 trillion to heirs and charities. Furthermore, a significant portion of this wealth is currently held in IRA’s and other retirement accounts that typically pass directly to designated beneficiaries. While the IRA distribution rules and tax consequences that apply during a taxpayer’s life are fairly straightforward, the complex distribution rules associated with inherited IRA’s are often overlooked and the consequences for not following them can be costly. If you recently inherited a Traditional IRA (pre-tax) or are currently listed as a beneficiary, it’s crucial that you understand all the distribution options available to you and how they differ based on factors such as the original account owners age, your relationship to them, and the type of IRA (Traditional or Roth).

*Note: The above distribution rules only apply to beneficiaries of Traditional (pre-tax) IRAs where the account owner passed away on or after January 1, 2020. Beneficiaries of Roth IRAs and accounts where the owner passed away before January 1, 2020 are typically subject to different distribution rules.

While an inherited Traditional IRA can be a major windfall, the rules surrounding your distribution options entail caveats and are much more complicated than what we’ve covered. In addition, it’s important for beneficiaries to take into account the tax implications of each option to ensure they receive the maximum benefit possible. For that reason, we highly recommend speaking with a tax or CERTIFIED FINANCIAL PLANNER™ professional who can help you review all your options and select the strategy that is best for your specific situation.

If you have questions or would like to discuss any of the information contained here in greater detail, please do not hesitate to contact us.

Sincerely,

AJ, Ryan, Gary, Rhonda and Tom

AJ Gilbert, CFP®

Ryan McCafferty, CFP®

Gary Fortier, CPA

Rhonda Gilbert, CPA

Tom Savage, CPA

Disclosures

Keystone Financial Group, Inc. does not provide legal or tax advice

The contents of this email and any attachments are confidential and intended for the named recipient(s) only. If you are not the intended recipient(s) (or have received this email in error) please notify the sender immediately and destroy this email. Any unauthorized copying, forwarding, disclosure, or distribution of the material in this email is strictly prohibited.

The indices mentioned are not managed and cannot be invested in directly. Past performance does not guarantee future results. Diversification and asset allocation strategies do not assure a profit or protect against loss.

Sources used for the article:

- *Global Markets Quarterly Update – T. Rowe Price Investment Research

- *Quarterly Market Review – J.P. Morgan Investment Research

- *Retirement Topics – Beneficiary, Internal Revenue Service (IRS)